There are many different investing paths to choose from like day trading, options trading, swing trading, value investing, growth investing and lots of others. For myself and many others, including Warren Buffet whose portfolio is roughly 90% dividend stocks, dividend growth investing is a style that we like to incorporate. Before we jump into dividends and dividend growth investing it’s important to understand a few things that are involved.

What Are Dividends?

A dividend is an amount of money that is paid by a company to its shareholders. An investor will receive a specified amount of money for each share that they own. For example, if you own 10 shares of Company A who announces a $1.00 dividend you will receive $10.00 on the date specified. Dividends are usually paid on a quarterly basis but they can also be paid monthly or semi-annually. Dividend payments can range anywhere from less than 1% to upwards of 20% of the share price. Though, companies that have a high dividend yield may not be able to sustain such a payment, choosing stocks solely on their dividend yield is extremely risky and not advised.

Three Types Of Dividends

There are three types of dividend payments you may receive, cash, stock and extraordinary. The most common type, a cash dividend is simply what it states, a payment from a company in the form of cash. A stock dividend is similar to a cash dividend except instead of paying shareholders with cash, they are paid with partial or whole shares of the company’s stock. An extraordinary dividend is a one time distribution of cash or stock to shareholders. This is also referred to as a “special dividend.” These dividends usually occur if a company makes an exceptional profit during a quarter or period.

Record Date and Ex-Dividend Date

The record date is the date announced by a company to determine which shareholders are eligible to receive a dividend. The ex-dividend date is usually set two days before the record date and it is the date in which you must own shares of a company in order to receive a dividend. If you purchase a stock on its ex-dividend date or after, you won’t be eligible to receive the most recently declared dividend. As long as you own a stock on the ex-dividend date you’re entitled to the dividend payout even if you sell your shares after the ex-dividend date. Buying a stock before its ex-dividend date and then selling after (but before the dividend payment date) and still receiving the dividend is called the dividend capture strategy.

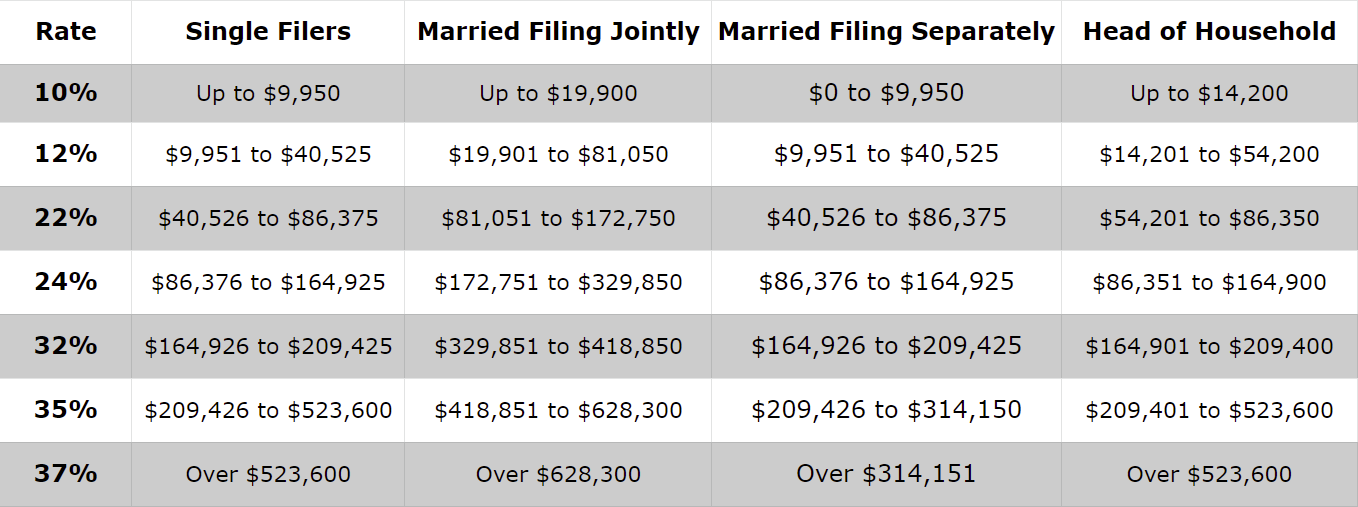

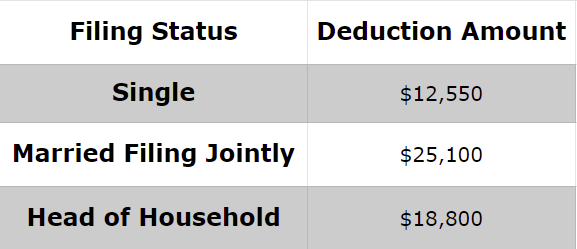

Tax Advantages

It is important to know that long term capital gains are taxed differently than short term gains or ordinary income. A long term investment is one that has been held for longer than one year. The personal income tax rate is usually significantly higher than the long term investment tax rate, as you can see by the chart. Long term investments can save you big come tax time and that’s one of the biggest benefits of dividend growth investing. Disclaimer: Non-qualified dividends come from REITs, MLPs, tax-exempt corporations, and foreign corporations. These non-qualified dividends are taxed at your personal tax rate rather than the long term investment rate.

Dividend Aristocrats and Dividend Kings

Aristocrats and Kings are a great place to begin researching stocks for your own dividend growth portfolio. Dividend Aristocrats are companies within the S&P 500 that have been paying an increasing dividend for at least 25 consecutive years. Dividend Kings are companies within the S&P 500 that have been paying an increasing dividend for at least 50 consecutive years. It is important to note that since 1930 roughly 40% of the total U.S. stock market returns have come from dividends.

What Is Dividend Growth Investing?

Dividend growth investing is a form of investing that focuses on dividend growth, obviously right? Obvious indeed, but the uniqueness of this style of investing is what is so intriguing. Let’s go back to the previous example with 10 shares of Company A. They were paying a $1.00 per share dividend. Assuming Company A increased their dividend by 5% for 10 years, the initial $10.00 received in dividends would have grown to $16.30. You didn’t have to invest any additional principal to receive the extra dividends and you likely would have seen share price growth as well. This is a small scale example for simplicity sake but it properly illustrates the premise of dividend growth investing. This is the unique compounding effect of dividend growth investing.

Long Term Approach and DRIP

A dividend growth strategy is a long term approach to investing. There are many benefits to this, including the tax benefits we talked about earlier. You can also plan on paying less in broker fees because you’ll be buying and selling much less frequently. Historically, dividend stocks tend to do much better than their non-dividend paying counterparts during a down market as well. In a dividend growth approach, a pull-back in the market usually means discounted stock prices and a prime buying opportunity.

When you sign up with a broker you usually have the option to enroll in a dividend reinvestment plan (DRIP). This means that when you receive a dividend payment it will automatically be used to purchase fractional or whole shares of the company that paid you the dividend. The alternative is that your cash will sit in your account until you manually reinvest it or withdraw it.

A DRIP can be advantageous as time is always a factor, but there is another option to consider as well. For example, you receive a dividend from a company whose stock price is at an all time high. Is it really the best time to invest more money into that company? Maybe it is, maybe it isn’t. There’s really no way to know for sure, but an alternative to this method is to receive your dividend payments and manually redistribute them into stocks that are valued better at that time. It does take more work but, the payoff can certainly make it worth it.

Consistent Income

Another advantage to dividend growth investing is the income. With a non-dividend paying stock you only have one way to make or lose money, capital gains or capital losses. Thus, the only way to receive money that you can use is to sell your shares for a capital gain. You will receive dividends without having to sell shares making it easy to get some money out of the market.

How To Calculate Yield

It’s fairly simple to calculate dividend yield once you get the hang of it. The yield of a stock is the return paid over one year. For a dividend stock that pays quarterly, the yield is the sum of the last four quarterly dividends, divided by the price of the stock, multiplied by 100. For example, let ‘s say you buy AT&T (T) at $42.00 per share. And the last four quarterly dividends have been $0.48, $0.48, $0.48 and $0.48 giving a total of $1.92 per share. 1.92/42 = 0.04571429. Multiplied by 100 gives you a 4.57% yield.

How To Pick Dividend Stocks

You can use lots of different methods to pick dividend paying stocks. Here are four common methods to evaluate dividend stocks. Free cash flow to equity, dividend payout ratio, dividend coverage ratio and the net debt to EBITDA ratio. Together they combine to form a solid method for picking dividend stocks to purchase. However, there are other factors to consider as well such as current price and market conditions.

Some Things To Be Aware Of

Be aware that companies do not have to continue to pay dividends and they can be cut at any time. In economic hardships, dividends are usually the first thing to go, or at least the first thing to be trimmed. This is probably the biggest risk involved with dividend growth investing. This highlights why chasing yield can be dangerous. High yield is appealing and for good reason, but it’s far from safe. If you plan on investing in a company that pays a high yield do your due diligence. Properly value that company to be sure that dividend is sustainable. Also be aware that in a rising interest rate environment, dividend paying stocks may drop in price. People will often turn to other investment options such as CDs or bonds.

What’s your take on dividend growth investing?